Nigeria’s economic recovery stumbled in April as surging fuel costs and Middle East tensions pushed private sector activity into contraction for the first time in 16 months.

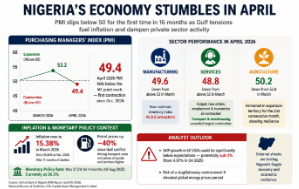

The West African giant’s Purchasing Managers’ Index (PMI), a key gauge of business activity compiled by the Central Bank of Nigeria, fell sharply to 49.4 in April from 53.2 in March, slipping below the critical 50-point threshold that separates expansion from contraction.

The decline, detailed in the central bank’s latest report released on April 29, marked the first contraction since December 2024 and underscored how vulnerable Africa’s largest oil producer remains to external shocks despite months of monetary tightening and fragile macroeconomic stabilisation.

The central bank blamed the downturn on “heightened geopolitical uncertainties and risk tensions in the Middle East”, a reference to the Gulf conflict that has disrupted energy markets and triggered fresh inflationary pressures across import-dependent economies.

The figures paint a worrying picture for President Bola Ahmed Tinubu’s administration, which has spent much of the past year trying to stabilise the naira, tame inflation and restore investor confidence after painful economic reforms, including fuel subsidy removals and currency liberalisation.

The contraction was most severe in the services sector, where the index dropped to 48.8 from above 52 in March. Manufacturing also weakened sharply to 49.6, while agriculture — though slowing from 52.8 to 50.2 — remained marginally in expansion territory.

The relative resilience of agriculture offered one of the few bright spots in an increasingly pressured economy.

Industry and services led the downturn, with transport and warehousing recording the steepest declines as fuel prices surged and logistics costs intensified. In manufacturing, the raw materials inventory index contracted to 46.8, reflecting weaker production activity and declining demand. The downturn also coincided with the end of an 11-month disinflationary trend.

According to figures released earlier by the National Bureau of Statistics, inflation rose to 15.38% in March from 15.06% in February, reversing months of gradual easing after inflation peaked at 34.8% in December 2024.

Economists say the renewed inflationary pressures reveal how deeply exposed Nigeria’s economy remains to imported energy shocks despite being one of Africa’s largest crude producers.

Petrol prices have reportedly climbed by around 40% since the outbreak of the Gulf conflict, triggering higher transport fares and rising costs of goods and services nationwide. For millions of Nigerians already battling a cost-of-living crisis, the renewed pressure has deepened anxieties over wages, food prices, and business survival.

Energy shock rattles fragile recovery

The latest PMI figures also raise difficult questions about the effectiveness of Nigeria’s aggressive monetary tightening cycle.

The Central Bank of Nigeria had raised its Monetary Policy Rate to as high as 27.5% for nine months until August 2025 before easing slightly to the current 26.5%, part of efforts to rein in inflation and stabilise financial markets.

While the tightening initially helped cool inflationary momentum, analysts warn that external pressures — particularly energy price volatility — are now overwhelming those gains.

Lagos-based VNL Capital Asset Management Limited warned that the contraction could significantly weaken first-quarter economic growth and potentially push the country toward stagflation — the toxic combination of rising prices and slowing growth.

“This also suggests that Nigeria’s GDP growth in Q1 2026 could come in significantly below expectations (potentially sub-3%, from 4.07% in Q4 2025),” the firm said.

“More importantly, it raises the risk that the economy may be drifting toward a stagflationary environment if elevated global energy prices persist.”

That warning is likely to resonate strongly among investors already watching Nigeria’s reform trajectory closely.

Tinubu’s government has sought to position itself as market-friendly, pushing through controversial reforms aimed at restoring fiscal credibility and attracting foreign investment. But the latest data highlights the structural contradictions at the centre of Nigeria’s economy: an oil-rich country still acutely vulnerable to imported fuel costs, supply disruptions and currency instability.

Analysts say the renewed economic strain could further complicate efforts to sustain growth in sectors outside oil, particularly manufacturing and transport, where operating costs remain highly sensitive to energy prices.

Businesses are also becoming increasingly cautious about investment decisions as uncertainty grows around inflation, consumer demand, and financing costs.

The PMI contraction may ultimately prove temporary if global tensions ease and fuel prices stabilise. But economists warn that prolonged geopolitical instability could deepen pressure on household spending, weaken industrial output and slow Nigeria’s broader recovery momentum.

For now, April’s figures offer a stark reminder that Nigeria’s fragile recovery remains tightly tied to events far beyond its borders — and that even after months of reforms and tightening, Africa’s biggest economy is still struggling to insulate itself from global shocks.

{kind=link}